Insurance & Investments Vol. 3

Permanent Life Insurance vs. Term Life Insurance: Which One Is Right for You?

When it comes to protecting your family’s financial future, life insurance is one of the most important decisions you’ll make. However, many people find themselves asking the same question: Should I choose Term Life Insurance or Permanent Life Insurance?

The answer depends on your financial goals, your stage of life, and the level of protection you need. Understanding the differences can help you make an informed decision.

What is Term Life Insurance?

Term Life Insurance provides coverage for a specific period of time—typically 10, 20, or 30 years. If the insured passes away during the term, the beneficiaries receive the death benefit. If the policy expires and is not renewed or converted, the coverage ends.

Advantages of Term Insurance

- Lower premiums, especially for younger individuals

- Straightforward and easy to understand

- Ideal for protecting temporary financial obligations

- Excellent for young families, mortgages, and income replacement

Considerations

- Coverage eventually expires

- Premiums may increase upon renewal

- Builds no cash value

- May become expensive later in life when insurance is needed most

What is Permanent Life Insurance?

Permanent Life Insurance provides lifelong coverage as long as the required premiums are paid. In addition to the death benefit, many permanent policies accumulate cash value that grows over time on a tax-advantaged basis.

Common types include:

- Whole Life Insurance

- Universal Life Insurance

- Participating Whole Life

Advantages of Permanent Insurance

- Lifetime protection

- Cash value growth

- Tax-advantaged savings opportunities

- Can assist with estate planning

- Provides financial flexibility later in life

- Death benefit is generally paid regardless of when death occurs

Considerations

- Higher premiums than Term Insurance

- Longer-term financial commitment

- More product options requiring professional guidance

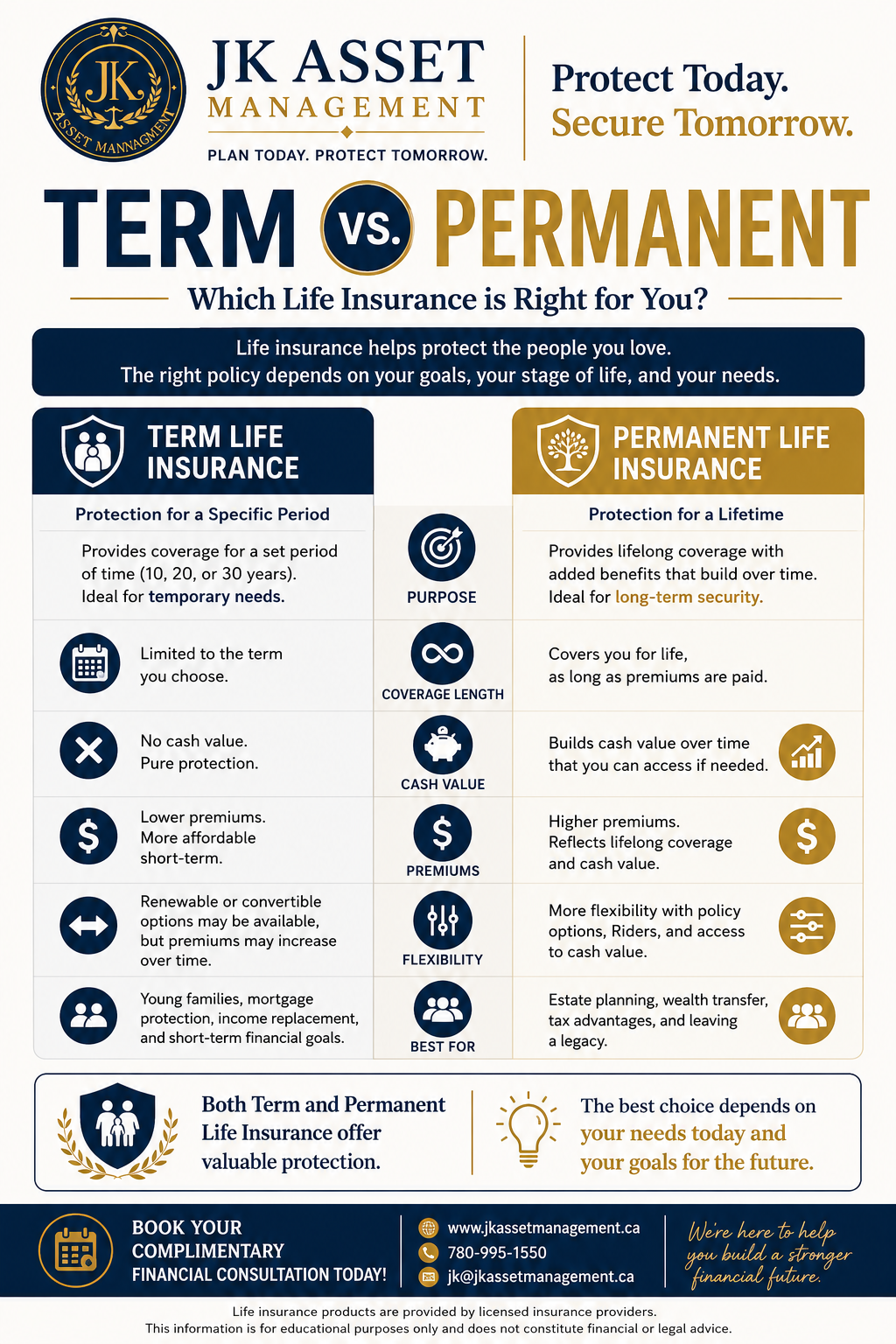

Comparing the Two

| Feature | Term Insurance | Permanent Insurance |

| Coverage Length | Fixed period (10–30 years) | Lifetime |

| Premium Cost | Lower | Higher |

| Cash Value | None | Yes (on many policies) |

| Death Benefit | During the term only | Lifetime |

| Best For | Temporary protection | Long-term financial planning |

Which One Should You Choose?

Term Insurance may be appropriate if you:

- Have a young family

- Need affordable protection

- Want coverage while paying off a mortgage

- Need income replacement during your working years

Permanent Insurance may be appropriate if you:

- Want lifelong protection

- Wish to build tax-advantaged cash value

- Are planning your estate

- Want insurance that can support long-term financial goals

- Desire coverage that won’t expire later in life

Can You Have Both?

Absolutely.

Many financial professionals recommend combining both types of insurance. For example, you might use:

- Term Insurance to provide affordable, high-value coverage while raising a family or paying down debt.

- Permanent Insurance to build long-term wealth, leave a legacy, or cover final expenses.

This layered approach provides flexibility while helping balance today’s budget with tomorrow’s financial goals.

The Bottom Line

There is no one-size-fits-all solution when it comes to life insurance. The right choice depends on your income, family situation, financial objectives, and long-term plans.

Rather than asking, “Which is better?”, consider asking:

“Which solution best fits my financial goals today and in the future?”

A personalized financial review can help determine the appropriate balance of protection and long-term planning for your unique circumstances.

Book Your Complimentary Financial Consultation

If you’d like to discuss your life insurance options and build a strategy tailored to your financial goals, I’d be happy to help.

📅 Schedule your complimentary consultation today:

https://calendly.com/kaplerjoseph

There’s no obligation—just an opportunity to gain clarity and make informed financial decisions for you and your family.

Joseph Kapler

Financial Advisor

JK Asset Management